When it comes to buying a home or refinancing a mortgage, it is crucial to pay attention to interest rates so you can budget accordingly. But what exactly drives those rates up or down? The Federal Reserve plays a significant role in shaping interest rates in the housing market, but there are other key factors that make an impact as well.

Let’s Dive A Little Deeper…

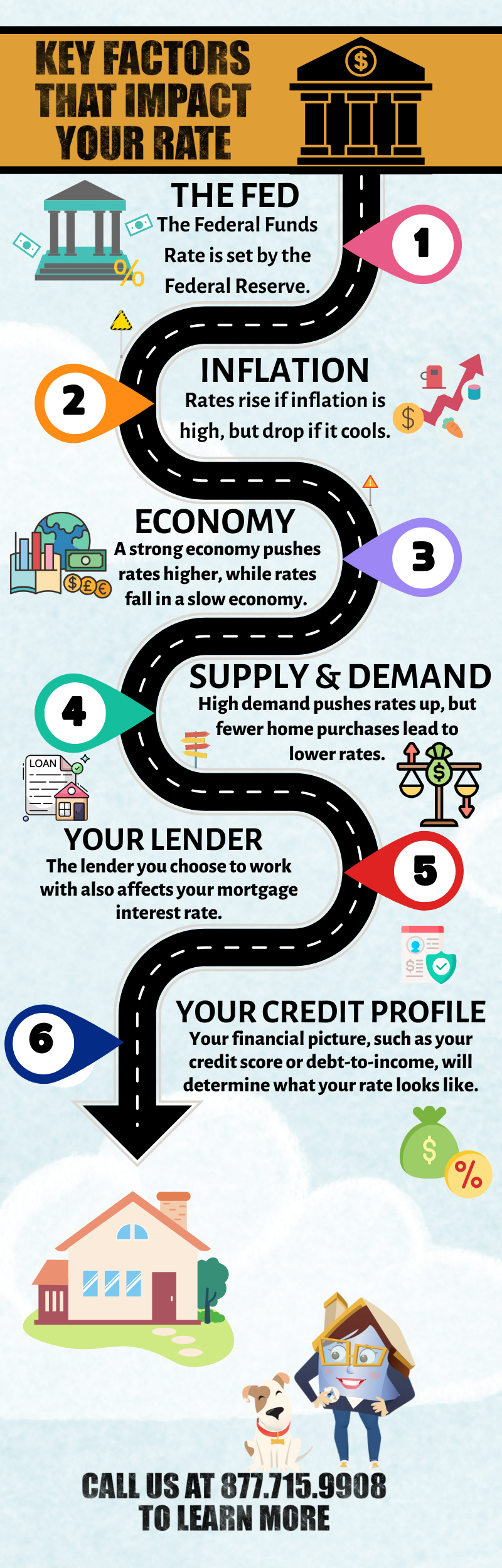

While The Fed doesn’t directly set mortgage rates, it does control something called the “federal funds rate,” which is the interest banks charge each other to borrow money.

So, how does this affect you?

If the federal funds rate goes up, it costs banks more to borrow money. As a result, mortgage rates typically go up too. If the federal funds rate goes down and it becomes cheaper for banks to lend money, mortgage rates will often go down.

But it’s not always that straightforward. After the Fed cut the federal funds rate in late 2024, for example, mortgage rates remained the same or increased slightly.

Why? Mortgage rates do not simply move in lockstep with the Fed (up when the Fed raises rates and down when it cuts them). Sometimes, mortgage rates move even before the Fed acts, because lenders are always trying to stay ahead of the game. There are also other factors at play, like the state of the economy, inflation and high demand for housing.

When the economy is strong, interest rates tend to rise. In contrast, rates typically fall during periods of economic slowdown. High inflation can also drive rates upward, as can strong demand in the housing market.

But that’s not all, the lender you choose and your personal credit profile can also affect your rate. Your financial picture, such as your credit score and debt-to-income ratio, will influence the mortgage rate you’re offered as well.

While the Fed’s decisions are a key piece of the puzzle, they’re not the whole picture. Understanding this dynamic can help you make more informed decisions when you hear about the next anticipated rate announcement, enabling you to navigate the housing market with the right expectations in mind.

Be sure to contact an AmeriHome Mortgage loan officer to ask about about current rates, and get your homebuying or refinance journey started with the information you need. Call us at 877.715.9908 to learn more.

Looking to start saving today on your home loan? Let’s upgrade your mortgage and put money back in your wallet with a new Purchase or Refinance Loan.*

6 Money-Saving Tips To Start Today:

| Pay Off Your Loan Sooner Switch to shorter loan terms to save on interest.* |

|

| Lower Your Monthly Payment Refinance with longer terms, so more money stays in your wallet.* |

|

| Consolidate Debt Cash-out to reduce high-interest credit card debt. |

|

| Pay For Larger Expenses Invest in your home with updates that will yield a higher return should you decide to sell in the future. |

|

| Get Extra Savings After you have financed a home with us once, save up to $750 on all your future refinances and new home purchase loans with your AmeriWallet Benefits.** |

If you are interested in learning more about how a refinance or new home purchase loan can benefit you, just give us a call at 877.715.9908 or get your instant rate quote here.

Imagine The Possibilities With Your Better Home Loan!

*By refinancing, your total finance charge could be higher over the life of the loan.

**As a member of the AmeriHome family, borrowers are part of the AmeriWallet Rewards program. If you completed a home loan with us once, you will qualify for a $750 lender credit for all of your future refinances or home purchases done with AmeriHome, for any property you own. To qualify for this offer, you must have previously financed the purchase of a home or refinanced with AmeriHome. You have financed with AmeriHome when AmeriHome Mortgage Company, LLC appears on the previous Promissory Note for your loan, and you are listed as a borrower on the Note. Credits will be applied only if your loan closes with AmeriHome. This offer can not be combined with any other offers and is not applicable for FHA Streamline, or VA IRRRL Refinance transactions. Other restrictions may apply. Terms and conditions are subject to change. AmeriWallet Rewards program is subject to termination without notice.